Blockchain Technology: A Complete Beginner’s Guide

Introduction Blockchain technology is one of the most revolutionary innovations of the 21st century. It has transformed the way we think about data, security, and digital transactions. Originally introduced in 2008 by an unknown person or group using the name Satoshi Nakamoto, blockchain was designed as the foundation for a new type of digital currency.

Blockchain technology is one of the most revolutionary innovations of the 21st century. It has transformed the way we think about data, security, and digital transactions. Originally introduced in 2008 by an unknown person or group using the name Satoshi Nakamoto, blockchain was designed as the foundation for a new type of digital currency.

At first, blockchain was only associated with cryptocurrency, especially Bitcoin. However, over time, it has evolved into a powerful technology that is now used in many industries such as finance, healthcare, supply chain, and more. Its ability to provide security, transparency, and decentralization makes it highly valuable in today’s digital world.

What is Blockchain?

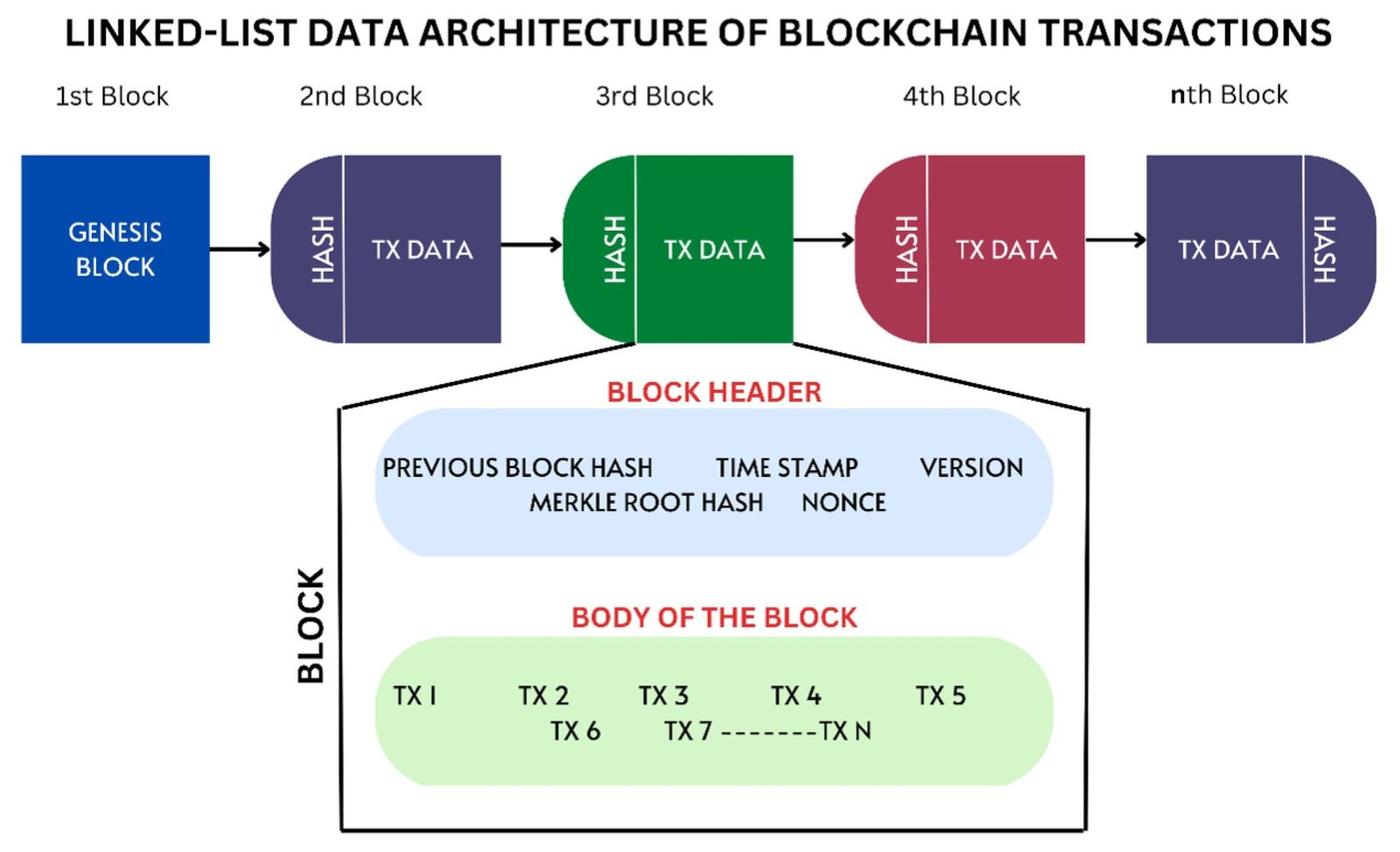

Blockchain is a digital ledger or record-keeping system that stores data in a secure and organized way. Instead of storing data in a single location, blockchain distributes it across a network of computers.

The term “blockchain” comes from two words:

- Block – A unit that stores data or transactions

- Chain – A sequence that links these blocks together

Each block contains:

- Transaction data

- A timestamp

- A unique code called a hash

Once a block is added to the chain, it becomes nearly impossible to change or delete. This makes blockchain a highly secure technology.

Origin of Blockchain

Blockchain was first introduced in a whitepaper titled

Bitcoin: A Peer-to-Peer Electronic Cash System

This document explained how people could send digital money directly to each other without relying on banks or financial institutions. This concept is known as a peer-to-peer (P2P) system.

The main goal was to create a system that is:

- Secure

- Transparent

- Independent of central authorities

This idea became the foundation of blockchain technology.

Blockchain and Bitcoin

Blockchain was originally developed to support Bitcoin, the world’s first cryptocurrency.

Bitcoin is a digital form of money that:

- Does not require a bank or government

- Allows direct online transactions

- Uses blockchain to store all transaction records

Every Bitcoin transaction is recorded on the blockchain, making it transparent and secure. Anyone can view the transactions, but the identity of users remains protected.

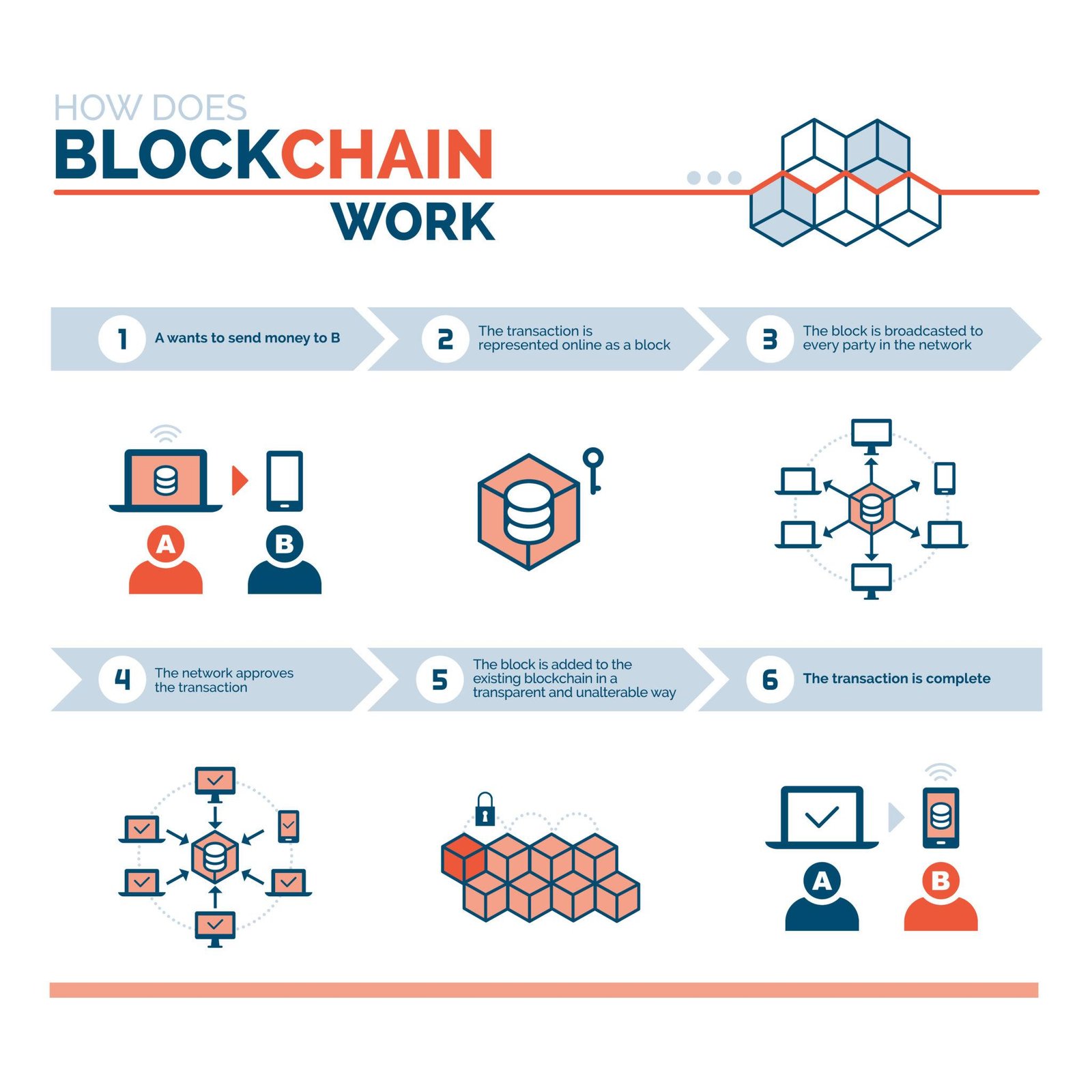

How Does Blockchain Work?

Blockchain works through a series of steps that ensure data security and accuracy:

- Transaction Initiation

A user requests a transaction, such as sending money or sharing data. - Verification

The transaction is verified by a network of computers called nodes. These nodes check whether the transaction is valid. - Block Creation

Once verified, the transaction is grouped with other transactions into a block. - Adding to the Chain

The block is added to the existing blockchain in a chronological order. - Completion

The transaction is completed and becomes permanent.

This process ensures that all records are secure and cannot be easily altered.

Key Features of Blockchain

1. Security

Blockchain uses advanced cryptography to protect data. Each block is connected using a unique hash, making it extremely difficult for hackers to change the information.

2. Transparency

All transactions are recorded on a public ledger that can be viewed by anyone in the network. This increases trust and reduces the chances of fraud.

3. Decentralization

Unlike traditional systems controlled by a central authority, blockchain operates on a decentralized network. No single entity has full control over the data.

4. Efficiency

Blockchain eliminates intermediaries such as banks, which speeds up transactions and reduces costs.

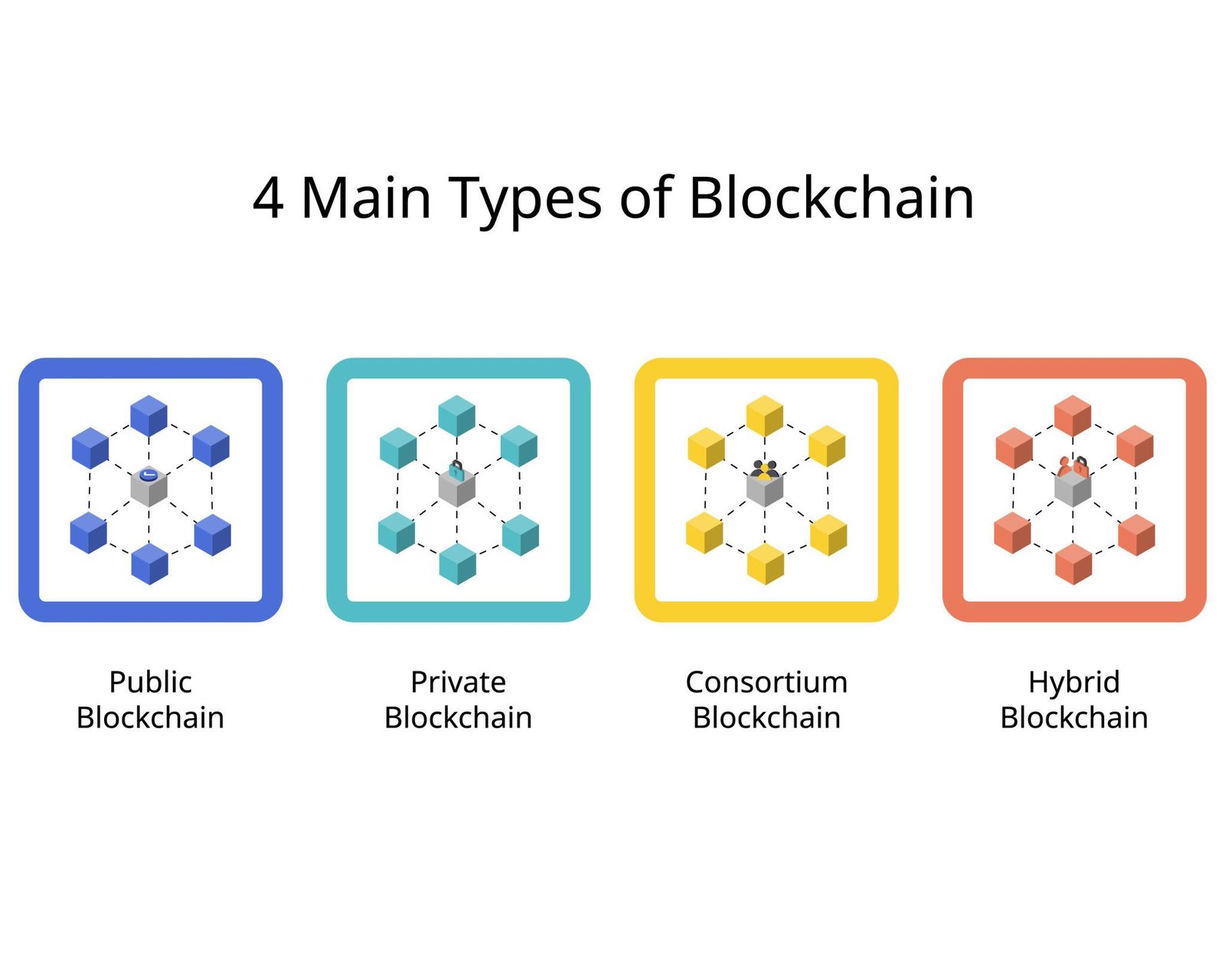

Types of Blockchain

There are different types of blockchain based on their usage:

- Public Blockchain

Open to everyone (e.g., Bitcoin) - Private Blockchain

Controlled by a single organization - Consortium Blockchain

Managed by a group of organizations - Hybrid Blockchain

Public plus private blockchain combined

Each type serves different purposes depending on the need for access and control.

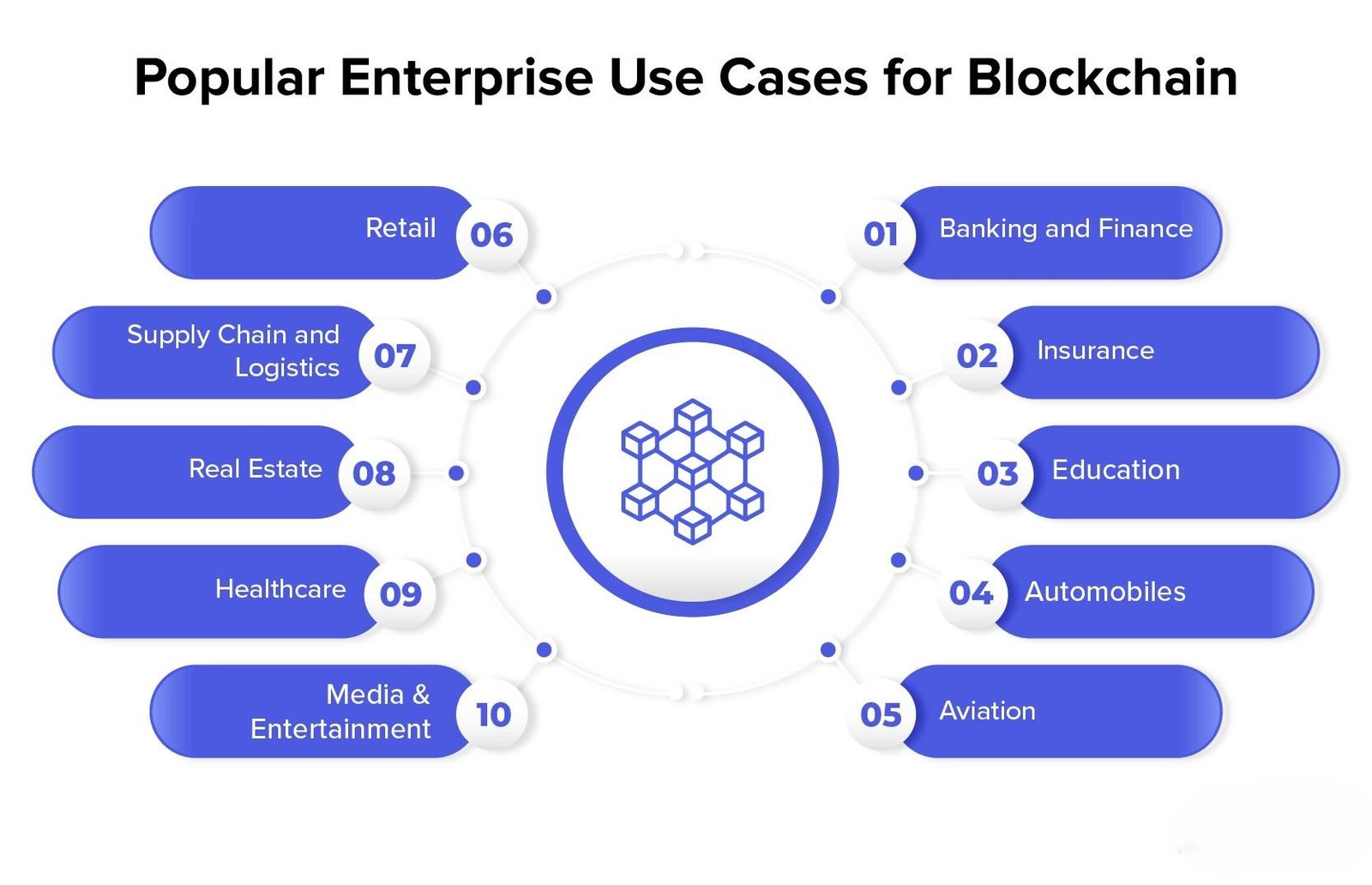

Applications of Blockchain Technology

1. Finance

Blockchain enables faster and cheaper money transfers. It reduces fraud and improves security in banking systems.

2. Supply Chain Management

Companies use blockchain to track products from production to delivery. This helps ensure product authenticity and transparency.

3. Healthcare

Blockchain allows secure storage of patient records. It also enables safe sharing of medical data between hospitals.

4. Voting Systems

Blockchain can be used to create secure and transparent voting systems, reducing the risk of election fraud.

5. Digital Identity

It helps individuals manage their digital identity securely without relying on third parties.

Advantages of Blockchain

- High Security – Data is protected using encryption

- Transparency – All transactions are visible

- Decentralization – No central authority

- Reduced Costs – Eliminates intermediaries

- Fast Transactions – Quick processing

Challenges of Blockchain

Despite its advantages, blockchain also has some limitations:

- High Energy Consumption

- Scalability Issues

- Complex Technology

- Regulatory Uncertainty

These challenges need to be addressed for wider adoption.

Future of Blockchain

The future of blockchain technology looks very promising. It is expected to play a major role in:

- Digital finance (DeFi)

- Smart contracts

- Internet security

- Data management

As technology continues to evolve, blockchain will likely become an essential part of everyday digital life.

Conclusion

Blockchain technology started as a system to support Bitcoin, but it has now grown into a powerful tool used across multiple industries. Its key features—security, transparency, decentralization, and efficiency—make it one of the most important technologies of the modern era.

As more organizations adopt blockchain, it will continue to transform the way we store and share information, making digital systems more secure and trustworthy.

“Im a senior developer, I search out the web3 and It was a very interesting topic”